Last data refresh: mid-June 2026 (FY2025 financial statements, released Feb 2026; FY2025 Annual Report). Price ~S$6.10. Figures approximate.

Sembcorp trades around S$6.10, on roughly 11× earnings and about a 4% yield, and is talked about as a green-energy transition story. The financial statements say something narrower: gas earns about three-quarters of group profit; renewables — the entire growth narrative and the largest call on capital — earns about a fifth. On a defensible cost of equity, my dividend model values the shares in the mid-S$6 range — around S$6.25 on flat growth, rising toward S$6.60 if I credit a modest near-term dividend lift — essentially fair, with the transition priced as a free option rather than a paid-for premium. The falsifiable claim: at today’s price the market is paying for the gas annuity, not the green build-out. What has to be true for that to be wrong is the subject of this piece.

New to reading SGX segment notes and cash-flow statements? Start with my guide: How to Read an SGX Annual Report.

Why This Matters Now

FY2025 results were solid enough on the surface. Group turnover came in around S$5.8 billion — down roughly 10% year-on-year, largely on lower gas generation volumes rather than a structural deterioration — while underlying profit held near S$1.0 billion and the return on equity stayed around 18%. The dividend was raised about 9% to 25 cents, a payout in the mid-40s percent of underlying earnings. These are not the numbers of a business in distress.

But two variables sit right at the pivot of whether that continues. The first is 2026 re-contracting. Sembcorp’s Singapore gas generation contracts roll at a time when pool electricity margins are under pressure. The affected capacity is a modest fraction of the overall portfolio — roughly 5% of direct exposure — but Sembcorp also has an interest in Senoko Energy, which adds further indirect weight to the same risk. Gas is where three-quarters of the earnings come from; any margin reset there flows straight through to the group profit line.

The second variable is Alinta Energy. Sembcorp’s Australian acquisition was expected to complete around the first half of 2026. It adds scale in a developed-market electricity system and, over time, another asset to the capital-recycling pipeline. It also adds leverage and integration complexity at a moment when the balance sheet is already carrying more weight than the headline gearing figure suggests — something I will come back to in the tensions section.

June 2026 also brings a board change: Andreas Sohmen-Pao becomes the non-executive, independent chairman. His background spans BW Group — where his remit encompassed leading a global business rooted in international energy and infrastructure — and the Global Centre for Maritime Decarbonisation: capital-intensive arenas where disciplined asset recycling is a survival skill rather than an optional strategy. I would not call the appointment a catalyst; governance continuity is probably the fairer interpretation. But it is at least a signal that the board is leaning into, rather than away from, the capital-discipline framing that the strategy depends on. Some observers will read this as neutral; I think that calibration is fair and worth stating.

The Earnings Question: Which Number Is Real?

FY2025 produces three different figures for attributable profit, and the spread matters for valuation.

Earnings reconciliation

| Measure | FY2025 (S$m) | EPS (S$) | Note |

|---|---|---|---|

| Reported attributable | 984 | 0.55 | incl. exceptional gains and an INR-driven DPN FX loss |

| Before exceptional items | 849 | 0.48 | strips one-off gains |

| Underlying | ~1,003 | ~0.56 | base case |

Sources: FY2025 financial statements; author’s normalisation.

The reported figure (~S$984 million) is the accounting total, but it contains a ghost worth naming: a non-cash foreign-exchange loss on Sembcorp’s Deferred Payment Note (DPN) from the 2023 sale of its India business. Sembcorp retained roughly S$1.3 billion of deferred consideration benchmarked to Indian government bond yields, so the note’s fair value moves with the rupee. In FY2025, the INR’s depreciation against the SGD drove an FX swing of about S$150 million into the P&L. This is not cash leaving the business; it is mark-to-market noise on a legacy asset. Reported earnings will keep absorbing INR/SGD movements until the note winds down — which is exactly why the underlying figure, with the DPN’s currency noise stripped out, gives the cleaner read of the go-forward energy business.

The before-exceptional figure (~S$849 million) goes the other direction, removing disposal gains that are real cash flows but not reliably repeatable at the same scale every year. Underlying (~S$1.0 billion, or about 56 cents per share) sits between the two: it adds back the DPN FX loss and removes the one-off disposal gains. That is my base case earnings figure.

The FCF-definition trap. There is a parallel ambiguity in cash flow that is worth flagging before we get to valuation. Sembcorp’s headline free cash flow figure — which the company sometimes cites at roughly S$2 billion — folds in asset-sale proceeds alongside operating cash generation. Strip those out and organic FCF (operating cash flow minus capex) is considerably thinner, in the couple-of-hundred-million range, because capital is flowing at pace toward the renewables build-out.

That gap between the headline figure and the organic figure is the reason I value this business on dividends rather than a discounted cash-flow model. A DCF would be hostage to assumptions about the build-out timeline and the eventual capex turn — assumptions with wide error bars at this stage of the transition. The dividend is covered on every definition of earnings (payout in the mid-40s percent) and is the most auditable number in the stack. That makes dividend discounting the defensible choice, not the lazy one.

Valuation: A Forward Read and a Reverse One

Before the model, a quick orientation on where the stock sits. Price ~S$6.10; market cap roughly S$10.9 billion; enterprise value roughly S$19 billion; net debt roughly S$7.8 billion; leverage ~3.9× adjusted EBITDA (or ~5.2× EBITDA excluding JV contributions — more on that distinction below); EV/EBITDA about 9–10×; PE roughly 11×; yield about 4%; price-to-book roughly 2×; ROE roughly 18%. Sources: SGX quote; FY2025 financial statements; author’s calculations.

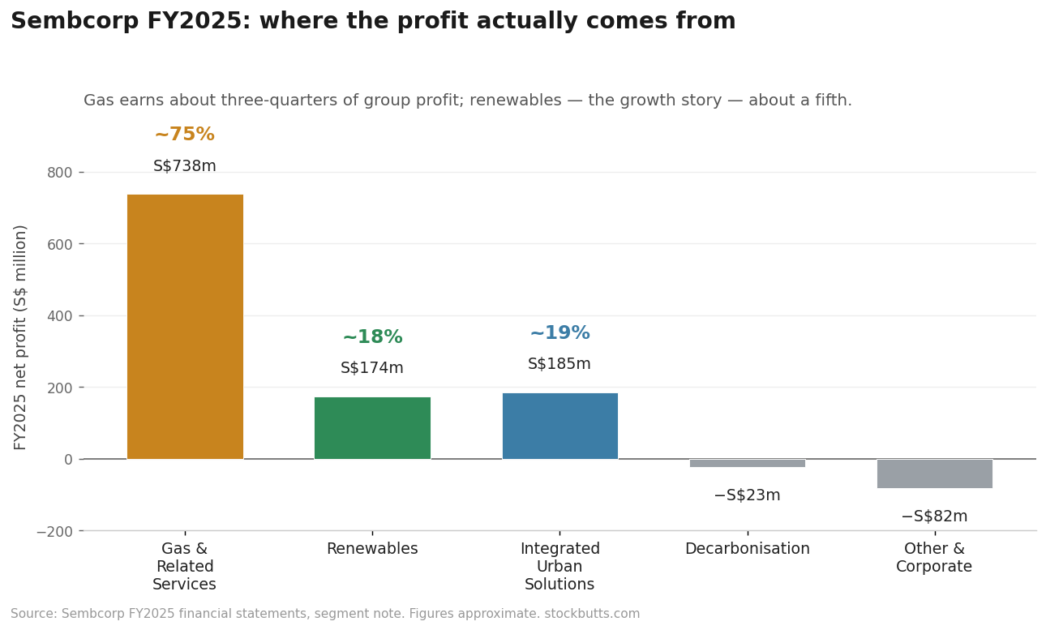

The segment picture behind those numbers is in the diagram below. Gas earns about three-quarters of group net profit. Renewables earns about a fifth. Integrated Urban Solutions also contributes about a fifth, while Decarbonisation Solutions and the corporate overhead are drags at the group level.

My approach is a dividend discount model. It is the cleanest lens for a capital-intensive group whose organic free cash flow is depressed by a build-out cycle that has not yet peaked. Cost of equity follows the standard build-up: the risk-free rate (about 2%, sourced from my earlier pillar on the Singapore risk-free rate — link), a 5% equity risk premium, and a beta.

I use 0.90 for the beta. That choice is worth a paragraph, because the screener on many retail platforms will tell you something very different — one popular tool reports a beta near 0.08 for Sembcorp. Plug 0.08 into the same formula and the implied cost of equity comes out below 2.5%. That is lower than Sembcorp’s own cost of debt. Equity investors do not accept a required return below the company’s senior creditors; the maths breaks at that point. A beta of 0.90 is defensible for a leveraged group with meaningful emerging-market and JV exposure operating through a capital-intensive transition. The gap between 0.08 and 0.90 is the difference between a stock that looks dramatically undervalued and one that is broadly fairly priced. The screener’s number is not a reason to buy; it is a reason to understand what the screener is actually doing.

On those inputs, the forward DDM puts fair value around S$6.25 on a flat-dividend assumption. Credit a modest near-term lift — consistent with management’s track record of steady dividend growth and the pipeline of contracted renewables capacity coming online — and the value rises toward S$6.60. Against a current price near S$6.10, that is broadly fair, with a slim transition premium the market is not explicitly paying for.

The reverse DDM. Rather than solving for value from my inputs, I can flip the question: what does the market have to believe for S$6.10 to be a fair price? The answer, from the reverse solve, is perpetual dividend growth of roughly 2.5% and a beta near 0.9 — almost precisely the assumptions I would choose independently. The market and my model converge. Sembcorp is priced as a mature, moderately risky income stock, with the entire renewables build-out offered close to free. That is either a gap waiting to close or an accurate reflection of execution risk. The tensions below explain which question to ask.

Part of what gives the renewables option some structural substance is contracted duration. New PPAs are being signed at multi-decade tenures — the deal with Meta Platforms, for instance, runs for 25 years. Set that against roughly half of Senoko’s gas capacity coming up for near-term re-contracting, and the contrast is instructive: the gas book faces near-term repricing risk while the new renewables agreements lock in revenues for a generation. Lower ROE, yes — but also structurally less exposed to margin resets.

Cross-checks. At about 9–10× EV/EBITDA, Sembcorp sits comfortably in the middle of the range for Asian utility and independent power producer peers. At roughly 11× earnings and ~4% yield it reads like a hybrid — income stock with a growth option attached. Both are consistent with the DDM range.

The ROE caveat. At roughly 2× book and an 18% ROE, a naive screen flags Sembcorp as cheap on a price-to-book basis. It is worth being careful here. Gas earns high returns; the existing renewables book earns lower, longer-duration contracted returns; the new capacity being built earns even lower rates in its early years. As the profit mix shifts from gas toward renewables, the blended group ROE falls — not because management is failing, but because that is the plan. Capital is being redeployed from a high-return legacy business into a lower-return, longer-duration one. The apparent gap between ROE and the cost of equity narrows, and with it the justified premium to book. Investors holding a view that the current 18% ROE represents a floor on the group’s long-run earnings quality are likely to be disappointed. That disappointment is already partly priced in; at 2× book rather than 3× or 4×, the market is not assuming the gas ROE persists forever. But it is worth being clear about what the number means. Readers who want a framework for thinking through when a declining ROE becomes a genuine bear case might find The Bear Case Habit useful.

Four Tensions the Market Must Resolve

Every valuation rests on assumptions. These are the four where I think the market’s current assessment is most likely to be tested.

1. Gas pays, green grows — but for how long?

Three-quarters of group profit comes from a fuel the world is committed to transitioning away from — though the customers matter as much as the fuel. According to the FY2025 Annual Report, Sembcorp supplies more than a third of total power demand for data centres in Singapore. The gas fleet underpinning that share is, for now, essential infrastructure for the economy’s fastest-growing demand source; it sits in a different transition bracket from coal or transport fuel. The question is not whether the long-run transition happens but whether the gas annuity holds its margin long enough, and at a level high enough, for renewables to mature into the earnings gap. The 2026 Singapore re-contracting is the first meaningful test. If gas margins compress significantly and stick there, base earnings reset and the dividend growth assumption in the model becomes harder to justify.

2. Two FCF numbers.

I flagged the organic-vs-headline FCF gap in the earnings section. Asset recycling at scale requires a willing buyer market, transaction execution, and disciplined reinvestment. Sembcorp has delivered on all three over recent years, which is what makes the track record relevant. But the Alinta acquisition adds a new asset to the portfolio that has to bed in before it can be recycled; it also consumes balance sheet capacity in the near term. The Sohmen-Pao appointment is the qualitative signal connecting to this tension — a chairman who has operated at the helm of a global energy and infrastructure group where asset recycling is the operating model, not a bolt-on, is consistent with the capital discipline the strategy requires. It does not guarantee execution.

3. An 18% ROE built to fall.

This follows directly from the segment mix. Renewables earn lower returns than gas. As capital allocation shifts, the blended ROE falls by design. That caps the justified earnings multiple over time. Investors anchoring to the current ROE as a baseline for future returns are working from the wrong starting point. This is not a critique of the strategy — lower-return, longer-duration contracted assets may well be the right place for capital in a decarbonising energy system. But it means the valuation today is partly a bet on the absolute level of future earnings rather than the current return profile.

4. Leverage into a transition.

The net debt of roughly S$7.8 billion looks moderate at ~3.9× adjusted EBITDA — but that adjusted figure includes the group’s proportionate share of JV earnings, while the debt sits at the parent level. Exclude the JV earnings and the same debt is ~5.2× EBITDA: the same obligation, against a smaller, wholly-controlled earnings base. That is the real margin-for-error figure — the one that matters when Alinta needs funding, the dividend needs to be sustained through a gas-margin reset, and the renewables capex programme continues to run. It is not a crisis level of leverage, but it is a constraint. Any scenario analysis that ignores the 5.2× figure and relies on the 3.9× one is flattering the balance sheet.

Risks: What Would Change My View

I try to pre-commit to the observable signals that would move my valuation before they happen. These are not forecasts; they are the conditions I have agreed to act on.

Bull case — toward S$6.60 and above.

Renewables net profit inflects up toward S$250 million or more as the roughly 15GW installed base matures — and does so without relying on disposal gains to get there. Gas margins hold through the 2026 Singapore re-contracting, keeping gas net profit broadly around S$700 million. Alinta integrates without a dilutive equity raise, and adjusted leverage trends below roughly 3.5× (with the ~5.2× ex-JV figure improving in parallel). If those three conditions are met within the next two or three years, I would revisit the growth assumption in the model and the valuation range shifts upward accordingly.

Bear case — toward S$6.25 or below.

Gas net profit falls below approximately S$600 million on a sustained basis in FY2026–27 — at that point the base earnings case resets and the dividend trajectory comes under pressure. Renewables net profit is flat or declining for two consecutive years despite rising installed capacity — that would be evidence that the growth narrative is not converting to earnings at scale, and I would stop crediting the transition premium and anchor on the flat-growth value. Or leverage deteriorates further rather than trending toward the targets above.

The Vietnam canary. One pre-observable, quantified risk worth isolating: Sembcorp’s Vietnam renewable joint venture has approximately S$33 million of carrying value already flagged as at risk from renewable-tariff policy changes, with up to roughly S$30 million of additional contingent exposure disclosed in the accounts. A crystallisation of that exposure — or comparable curtailment or tariff actions in China — would not by itself shift my group valuation materially. But it would be a live, measurable confirmation that regulatory risk in the build-out is real rather than theoretical. It would move my qualitative confidence in the regulatory sensitivity of the earnings assumptions. Watch the contingent-exposure note at each half-year and full-year result.

A final note on Alinta: once the acquisition completes and the first full contribution period is visible, it is worth re-running the base case. Both the earnings inputs and the leverage inputs will change; the rounded valuation range may shift in either direction depending on how the integration goes.

Closing Thought

Fairly valued is not the same as uninteresting. At around S$6.10, the price buys the gas annuity at a reasonable multiple and hands you the renewables build-out — the capex programme, the 15GW pipeline, the entire energy-transition narrative — at something close to zero incremental cost. Whether that is a gift or a fair reflection of execution risk is the real debate. It is a debate about discount rates and profit-mix trajectories, not a mispricing that a screener has surfaced.

For the transition premium to materialise and push the shares toward the upper end of my range, renewables need to start earning at a rate that justifies the capital deployed, the gas engine needs to hold long enough to fund the journey, and the leverage needs to trend in the right direction as Alinta beds in. None of those conditions is improbable. None of them is guaranteed. That is what fairly valued means.

Disclosure: At time of writing, the author holds no position in Sembcorp Industries (U96) and has no plans to initiate one within the next 72 hours. Figures in this article are approximate and rounded, reflecting data as at mid-June 2026; they illustrate valuation logic rather than precise point estimates.

Disclaimer: This article reflects the author’s personal analysis and opinions, written in a strictly personal capacity. It is not financial advice and does not take into account any individual reader’s financial situation, investment objectives, or risk tolerance. Information is sourced from publicly available filings as of the date noted but accuracy cannot be guaranteed. The author may hold positions in securities discussed (see disclosure above). Readers should conduct their own research and consider consulting a licensed financial adviser before making any investment decisions. The author is not a licensed financial adviser under the Financial Advisers Act of Singapore.

An ordinary man with extraordinary inspiration