Most stock analysis exists to sell a conclusion. The “undervalued gem” with a target price; the high-conviction call with no stated conditions. The format moves well — certainty feels like competence, and a clean call is easy to share. What it almost never does is say what “wrong” looks like. An argument that cannot be falsified is not a view; it is a conclusion in search of permission.

The discipline that separates analysis from advertising is the bear case: written deliberately, specifically, and before the bull case has had time to make you fall in love with it. Three habits follow from that single premise — write the bear case first; present a distribution rather than a single scenario; and state, in advance, what would change your mind.

The stakes are not abstract. In 2011, Hyflux won the bid to build Singapore’s largest desalination plant — Tuaspring, a 318,500 cubic-metre-per-day facility paired with a 411 MW power plant — at a water-supply price of S$0.45 per cubic metre. That figure was loss-making on its own. The model worked only if electricity sales from Tuaspring’s power segment cross-subsidised the water contract. The bull narrative — systemic infrastructure, Singapore state linkage, yield of up to 6% on perpetual securities and preference shares marketed as low-risk income — was easy to hold and structurally impossible to break. The specific bear question it foreclosed was precise: what happens to the whole structure if Tuaspring’s power economics turn negative?

From 2015, a generation-capacity glut drove Singapore’s wholesale electricity prices down by more than 50%. The cross-subsidy collapsed. In 2017, Hyflux recorded its first-ever net loss of S$115.6m; in 2018, it suspended trading on approximately S$2.9–3bn in debt. Around S$900m of retail capital from roughly 34,000 holders of perpetual securities and preference shares faced near-total losses. The power-price collapse was a market risk that materialised: generation oversupply was precisely the bear-case condition the bull narrative had foreclosed from examination. Without it, the story held right up until it did not.

That is the cost of an unfalsifiable bull case.

Falsifiability and the Asymmetry of Proof

Karl Popper’s contribution to the philosophy of science can be paraphrased in a sentence: a claim consistent with every possible outcome explains nothing. For a claim to be meaningful, there must exist, at least in principle, an observation that would prove it wrong. Most readers will recognise the standard from science. Fewer apply it to a stock pitch.

The application to investing is direct. A bull thesis that cannot name the observation that would refute it is not a thesis — it is a story. And the financial content industry generates stories at scale. The “undervalued gem” that is always compelling but never falsifiable; the conviction call that survives every counter-datapoint because the terms of the argument were never anchored to a specific, observable condition. The Hyflux bull narrative fits this pattern exactly: systemic, infrastructure-backed, yield-generating, difficult to attack in precise terms, and therefore never attacked in precise terms — until reality supplied the precision the analysis had withheld.

There is an asymmetry in how falsification works that shapes the construction of a bear case. A thousand quarters of good results cannot prove a bull thesis right — every good quarter is equally consistent with “this is a great business” and “this is a great business about to roll over.” The evidence accumulates, but it never delivers proof. A single structural shift, however, can prove the thesis wrong in one observation: when Tuaspring’s power economics turned negative, the cross-subsidy model was dead. One event, sufficient to invalidate the entire model.

This asymmetry is why the bear case is not a downside hedge bolted on after the bull thesis is complete. It is the boundary condition of the thesis itself — the line that, if crossed, ends the argument. Named in advance; not improvised after the fact. Most “bear cases” I see in online analysis do not function this way. They are downside scenarios — a P/E (price-to-earnings) ratio that implies a lower price — rather than a falsification condition: the specific observation that ends the thesis entirely.

Two frameworks sharpen this discipline. Munger’s inversion, paraphrased: rather than asking how a thesis succeeds, ask how it dies — then avoid the conditions that produce that outcome. The pre-mortem, from Gary Klein: before a position is taken, assume the position has already failed eighteen months from now and write the explanation of why. Both exercises force the bear case to the front of the analysis, where it belongs, rather than to the back matter, where it is usually filed.

Habit 1: Write the Bear Case First

The instruction is literal: before building the bull case, write down what kills it. Two separate arguments support why this sequence matters.

The first is about confirmation bias — the well-documented tendency to weigh evidence that supports an existing view more heavily than evidence that challenges it. Once you have decided you like a business, every additional piece of research becomes an opportunity to reinforce the view. Committing the disconfirming evidence to paper before you are emotionally long is an inoculation, not a guarantee. It does not prevent bias; it raises the temperature at which the bias takes hold.

The second argument is about the instrument. The cleanest bear-case generator is the reverse lens: asking not “what is this worth?” but “what does today’s price require this business to be?” The reverse price-to-book ratio — P/B, meaning share price divided by book value per share — implies a required long-run return on equity (ROE; net profit divided by shareholders’ equity) via the Gordon Growth Model. Instead of building a model to arrive at a price, the reverse P/B asks: given today’s P/B, what ROE must this business sustain indefinitely for the price to be justified? The price answers for itself; the analyst’s optimism is not invited.

I applied this to DBS in a published analysis. The initial read — an implied long-run ROE of 14.6% — looked like “quality bank at a fair price.” Then I caught an error in my risk-free rate assumption. I had used a Singapore government bond yield of 3.2% when 2.10% was the more defensible current figure. Correcting the input changed the cost of equity (Ke; the required return on the equity portion of capital, used to discount future earnings) from 7.45% to 6.35%. The implied long-run ROE fell from 14.6% to 11.9%, and the read flipped: not “quality at a fair price” but “the market is pricing pessimism about DBS’s ability to sustain peak-cycle returns.” I published the correction.

“When the numbers change, the valuation direction changes instantly—the ego stays out of the spreadsheet.”

A habit that produces defensible analysis only when you turn out to be right is not a discipline. It is luck wearing the costume of process.

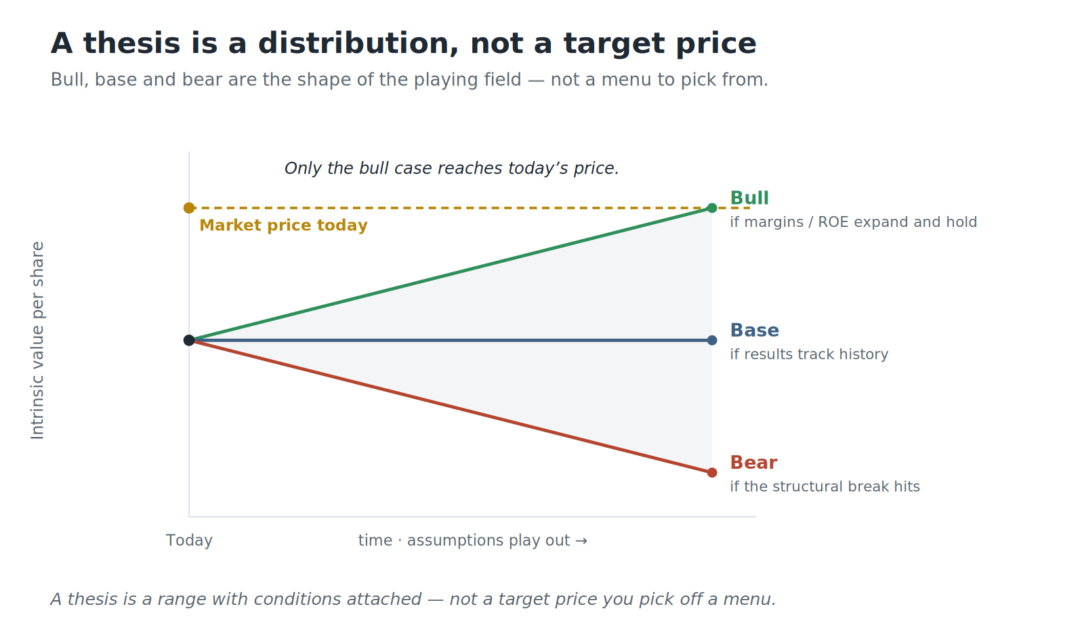

Habit 2: A Distribution, Not a Menu

The most common upgrade to a point-estimate valuation is bull/base/bear scenarios. The structure looks disciplined; the practice usually is not. Most people treat it as a restaurant menu: three options, one of which gets picked. And because the analyst built the model because they like the story, the bull case gets ordered.

Bull/base/bear is not a set of options to choose among. It is the entire shape of the playing field — the bounds within which the actual outcome will land if the analytical assumptions hold. The job is not to pick a scenario; it is to assess whether the current market price is mispricing the whole distribution.

In the DBS analysis, the scenarios span the current share price — bear cases landing close to it, bull cases extending to valuations no developed-market bank has sustained through a full economic cycle. Those bull figures are upper bounds, not targets — the ceiling of the distribution, defined by the conditions that would have to hold for them to be true. They constrain the analysis; they are not picks from the menu.

The OCBC analysis supplies a different version of the same argument: two internally consistent valuation methodologies with a wide gap between them. A dividend discount model (DDM — a framework that values a stock as the present value of its forecast dividends) implies a range of approximately S$19–21. A price-to-book framework implies S$25–47. The lazy move is to average the two. Averaged valuations are the investment equivalent of a weather forecast that says “somewhere between zero and 40 degrees, so let’s call it 20.” The honest move is to find the structural inconsistency that causes the divergence. The DDM and the P/B framework converge only when the implied long-run growth rate equals ROE multiplied by the earnings retention ratio — approximately 12.6% × 49% ≈ 6.2%, against the 2.5% terminal growth rate used in the DDM. That gap between 2.5% and 6.2% is the disagreement, quantified. Mapping it, rather than averaging it away, is what makes a scenario framework honest rather than decorative.

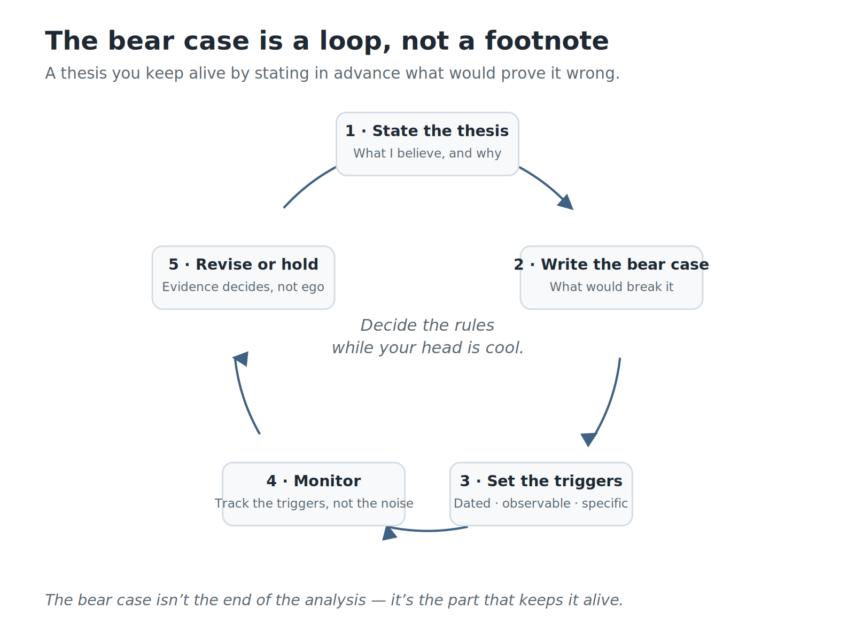

Habit 3: Say What Would Change Your Mind — In Advance

“A thesis without a dated, observable expiration date is a religious belief, not an investment.”

Pre-committing the revision triggers is the hardest of the three habits, because it constrains your future self. The bear case names what breaks the thesis. The revision triggers bind you to act when those conditions materialise. The gap between the two is where most analytical discipline fails.

The structural explanation is escalation of commitment — the tendency to double down when the evidence turns against you. The mechanism is not irrationality; it is sunk cost, ego investment, and the fact that judgment is worst under stress. The moments that most demand clear reassessment are also the moments when reassessment is most costly.

Writing the triggers in advance is a deliberate hack on this dynamic. The decision rule is constructed while the analyst’s head is cool and the position is not under pressure. When the market turns, the rule already exists. The cognitive task during the hard moment is not “should I revise?” — it is “did the condition I already specified actually materialise?” A much simpler question.

In the OCBC analysis, I hold approximately 1,100 shares and published five specific conditions that would prompt a revision, each tied to a metric, a threshold, and a results date. The market-implied ROE I read from OCBC’s current valuation is approximately 9.95%, against a recent realised ROE of 12–13% and a five-year average of approximately 12.1%. The thesis holds while that gap remains credible. The five conditions define precisely what “no longer credible” looks like. Holding a position and maintaining a live bear case are not in tension — the bear case is what keeps the holding intellectually honest rather than something I am now defending.

The Frencken analysis takes this to a natural conclusion. A reverse DCF — a discounted cash flow model (DCF; a valuation framework that converts forecast future cash flows into a present value) run backwards, with the current price treated as the answer and the implied assumptions as the question — produced a blue-sky valuation of approximately S$3.08 using optimistic, history-supported inputs including an 8% EBIT (earnings before interest and tax) margin and strong growth across both divisions. That figure was still approximately 2.1% below the S$3.15 close at the time of writing. For the market price to be justified, terminal growth would need to exceed 4% per annum — pricing a cyclical electronics manufacturer like a forever-growth software business. The maths supplies the falsification condition without further effort: if you believe the terminal growth assumption embedded in today’s price, you are holding a different business than the one in the financials.

Why This Is the Whole Brand

The bear-case habit is slower. It will never produce a “10x pick you cannot miss” headline. It costs the dopamine of the confident call, and it imposes a discipline that sometimes means publishing a correction, sometimes means holding a position in tension with its own disconfirming evidence, and always means saying precisely what “wrong” looks like before the fact rather than after.

What it buys is the only thing that matters on a site like this: the reader’s justified trust. Not trust that every analysis turns out to be correct — no system delivers that — but trust that the framework is honest about its own limits. A view that names its own falsification conditions can be evaluated, tracked against reality, and updated when reality speaks. That is a different product from a conclusion; it is more work to produce and more useful to read.

The practical takeaway is a demand, not a checklist. Make it of any investment analysis you read — including everything on this site. Does it name the conditions under which it is wrong? Does it present a distribution with boundary conditions, or a target price with no stated expiration? Does it pre-commit to revision, or reserve the right to explain away every bad quarter as a one-off? If the answers are no, you have a story. Stories are enjoyable. They should not be the basis for a capital allocation decision.

The method behind every article on stockbutts.com is the same one described here, and you can see it in practice in how I approach valuing a manufacturing company and reading an SGX annual report. The bear case comes first. It shapes everything after it.

Disclosure: The author holds a long position in OCBC (SGX: O39) — referenced here as an example, and the reason the author tracks the five specific conditions that would prove the thesis wrong. The author holds no position in DBS (D05) or Frencken (E28). This is a methodology essay, not a recommendation on any security.

Disclaimer: This article reflects the author’s personal analysis and opinions, written in a strictly personal capacity. It is not financial advice and does not take into account any individual reader’s financial situation, investment objectives, or risk tolerance. Information is sourced from publicly available filings as of the date noted but accuracy cannot be guaranteed. The author may hold positions in securities discussed (see disclosure above). Readers should conduct their own research and consider consulting a licensed financial adviser before making any investment decisions. The author is not a licensed financial adviser under the Financial Advisers Act of Singapore.

For the full site disclaimer, see the Disclaimer page.

An ordinary man with extraordinary inspiration